Upcoming Event

Free Newsletter

Free Newsletter

Markets rebound and economic indicators hold steady as Trump’s ceasefire signals shape outlook on growth and stability. (Photo/DepositPhotos)

Markets rebound and economic indicators hold steady as Trump’s ceasefire signals shape outlook on growth and stability. (Photo/DepositPhotos)

Resilience in uncertain times: the US economy holds

Stephen Slifer // April 23, 2026//

- Trump signals mixed messaging on Iran but ceasefire suggests push for stability

- S&P 500 rebounds sharply and nears record highs despite volatility

- GDP impacted by shutdown, underlying growth closer to 1.5-2.0%

- Labor market remains strong with unemployment at 4.3%

Early this month President Trump said that “a whole civilization will die tomorrow” if Iran failed to meet his deadline to reopen the Strait of Hormuz. A day later he announced a 14-day ceasefire. Huh? What does he really want? War? Or peace?

While those two statements may seem confusing, to us they are simply Trump being Trump. It is his negotiating style. Keep people off balance. Be unpredictable. In this particular case we believe that he truly wants the war to end. Our reason has nothing to do with the war itself. It is based on the fact that the midterm elections are seven months away with a lot of campaigning that must take place in the interim.

While those two statements may seem confusing, to us they are simply Trump being Trump. It is his negotiating style. Keep people off balance. Be unpredictable. In this particular case we believe that he truly wants the war to end. Our reason has nothing to do with the war itself. It is based on the fact that the midterm elections are seven months away with a lot of campaigning that must take place in the interim.

Republican candidates will have a hard time convincing voters to reelect them if the fighting continues and gas prices remain above $4 per gallon. The cease fire may hold, but it will likely be a rocky road to peace. There will be regular skirmishes along the way and the rhetoric will be as acerbic as always. Nevertheless, we believe that the end is in sight.

It would appear that stock market investors agree with us. After plunging by 10% the S&P 500 has rebounded sharply and is currently 1.4% below the record high level set in mid-January. Given the volatility in recent weeks it feels like the stock market should be down by 10% or more. It isn’t. In fact, it is one good day away from a record high level. How can that be? We think it is largely because of the resilience of the U.S. economy.

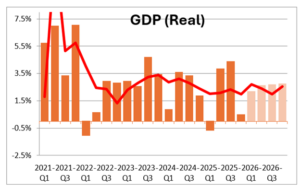

For example, fourth quarter GDP growth was reported to be a meager 0.4%. But the six-week government shutdown that occurred in that quarter snarled air traffic, closed national parks, dampened tourism, furloughed thousands of federal employees and forced others to work without pay.

The Bureau of Economic Analysis said that the shutdown reduced GDP growth in that quarter by 1.2%. In other words, if the shutdown had not occurred the BEA suggests that GDP growth would have been 1.6%.

Then there is an alternative measure of economic activity in any given quarter known as “gross domestic income” or GDI. In theory, GDP and GDI should be identical because one measures the economy from the production side, the other from the income side. But they never are the same because they are derived from different sources.

GDI rose a solid 2.6% in the fourth quarter. The bottom line is that the government shutdown sharply reduced GDP growth in the fourth quarter and had it not occurred growth both GDP and GDP would probably have been in a range between 1.5-2.0%. Not great, but certainly not the near 0% growth that was reported.

Looking ahead to the first quarter we estimate GDP growth of 2.0%. The consensus appears to be roughly comparable at 1.8%. In either case, growth appears to have been moderate. But given everything that the economy has gone through, we find that growth rate impressive. Think about it. Businesses are still figuring out ways to adapt to the tariffs Trump imposed last year.

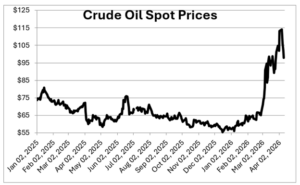

They are modifying their supply chains. Three-hundred-fifty thousand federal government workers were laid off last year and have had to seek jobs in the private sector. The federal government shut down for six weeks. The U.S. and Israel began a war with Iran in late February and oil prices have surged to $115 per barrel.

In ordinary times that combination of events should have caused consumers to sharply curtail spending and businesses to halt all new investment and lay off tens of thousands of workers. But that hasn’t happened. Instead, the economy still seems to be chugging along at a 1.5-2.0% pace despite these headwinds.

In ordinary times that combination of events should have caused consumers to sharply curtail spending and businesses to halt all new investment and lay off tens of thousands of workers. But that hasn’t happened. Instead, the economy still seems to be chugging along at a 1.5-2.0% pace despite these headwinds.

In the labor market payroll employment has slowed but mass layoffs have not occurred. At the same time fewer people need jobs because the labor force has stopped growing. As a result, the unemployment rate is 4.3% which basically means that everybody who wants a job still has one. In the fall the Fed cut rates twice because it feared the labor market would soften quickly. So where is the weakness? Once again, the economy is holding together nicely and defying the pessimists.

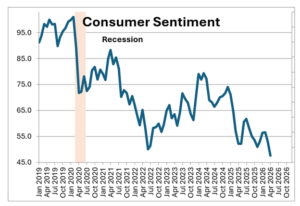

Could all those bad things be just over the horizon and clobber growth in the spring and summer months? Sure? But that is not our call. We believe the worst is over. If the cease fire generally holds together with only a few hiccoughs along the way, consumer and business sentiment should rise.

From 1980 until his retirement in 2003, Stephen Slifer served as chief U.S. economist for Lehman Brothers in New York City, directing the firm’s U.S. economics group along with being responsible for forecasts and analysis of the U.S. economy. He has written two books on using economic indicators to forecast financial moves and previously served as a senior economist at the Board of Governors of the Federal Reserve in Washington, D.C. Slifer can be reached at www.numbernomics.com.