Upcoming Event

Free Newsletter

Free Newsletter

(Photo/DepositPhotos)

(Photo/DepositPhotos)

Volatility reigns as war clouds economic forecasts

Stephen Slifer // April 14, 2026//

A month into the fighting, it is hard to see how the war can end soon despite Trump’s assurances that it is almost over. Iran’s missile arsenal has undoubtedly shrunk, but it is not depleted. Iran still poses enough of a threat to keep the Strait of Hormuz effectively closed and the country still inflicts significant damage to most of its Gulf neighbors.

A month into the fighting, it is hard to see how the war can end soon despite Trump’s assurances that it is almost over. Iran’s missile arsenal has undoubtedly shrunk, but it is not depleted. Iran still poses enough of a threat to keep the Strait of Hormuz effectively closed and the country still inflicts significant damage to most of its Gulf neighbors.

Economists and market participants keep searching for signs that a near-term end is in sight, but they are becoming increasingly frustrated. Whenever the stock market is poised to collapse, Trump says something positive, triggering a significan rebound. A day or two later, when there is still no progress on ending the war either militarily or via negotiations, the downslide resumes.

This optimism-pessimism flip-flop has created considerable volatility in the stock, bond and oil markets. Market movements are driven almost entirely by headlines about the war or oil. The underlying economy is irrelevant for now.

Everybody needs to know what’s next and that is largely a guessing game which nobody can predict with any level of confidence.

The S&P 500 index has fallen about 8% from its peak, which is still relatively modest. But it feels like it has declined at least twice as much because of the volatility.

The VIX volatility index has risen sharply since the war broke out, but it is not nearly as high as it was a year ago when widespread tariffs were imposed.

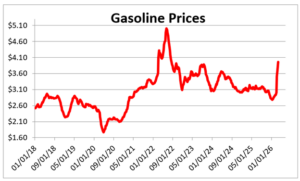

The war has had its most significant impact on oil prices. At the end of last year, West Texas Intermediate crude was about $57 per barrel. Today, it is 70% higher at $97.

That has boosted gasoline prices up 40%, from $2.81 per gallon to $3.96. That matters as consumers are spending more to fill the car with gas, leaving less money to spend on everything else.

The yield on the 10-year Treasury note has climbed from 4.0% at the end of last year to 4.4%.

The rise in the 10-year yield has boosted 30-year mortgage rates from 6.0% a month ago to 6.4%. The housing market had been showing signs of an incipient rebound in recent months as affordability improved. But 6.4% mortgage rates may well short-circuit the recovery.

Clearly, higher oil prices, higher bond and mortgage rates, and a drop in stock valuations will weaken GDP growth and boost inflation in the near term, but what happens next? Most economists and market participants cannot see a near-term end to the war, but what if President Trump declares victory and ends the war tomorrow? That would certainly help the near-term outlook for all markets, but ending the war prematurely would most likely lead to another round of hostilities at some point down the road.

However, ending the war prematurely could lead to renewed hostilities later.

For what it’s worth, traders expect West Texas Intermediate oil to fall from $97 per barrel today to $78 by year-end. That is a significant drop but still well above the $57 price that existed at the end of last year.

A drop of that magnitude should keep the inflation rate and bond yields fairly steady. Mortgage rates may return to the 6% mark. Against this background the Fed will probably hold the funds rate at its current level of 3.6% through the end of the year (despite a new chairman).

At the end of last year, we expected vibrant 2.9% growth for 2026. Given all of the above we may reduce tha to 2.2%, which is still acceptable, but not nearly as robust as it might have been in the absence of war.

And the inflation rate should remain at about the 3% mark rather than dipping to 2.7% as we anticipated at the end of last year.

But it is hard to have confidence in any forecast. Look what has happened in the first three months of the year? At this point any forecast — including ours — is nothing more than a guess dependent upon the degree of optimism or pessimism about the war. It is easy to come up with a very gloomy outlook, but Trump can produce surprises.

From 1980 until his retirement in 2003, Stephen Slifer served as chief U.S. economist for Lehman Brothers in New York City, directing the firm’s U.S. economics group along with being responsible for forecasts and analysis of the U.S. economy. He has written two books on using economic indicators to forecast financial moves and previously served as a senior economist at the Board of Governors of the Federal Reserve in Washington, D.C. Slifer can be reached at www.numbernomics.com.

C