Upcoming Event

Free Newsletter

Free Newsletter

(Photo/DepositPhotos)

(Photo/DepositPhotos)

May jobs growth fuels Fed rate hike concerns

Stephen Slifer // June 11, 2026//

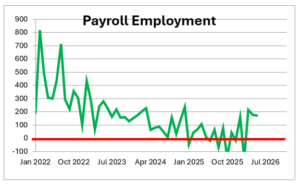

- Payroll employment increased by 172,000 in May, with three-month average gains of 188,000 jobs.

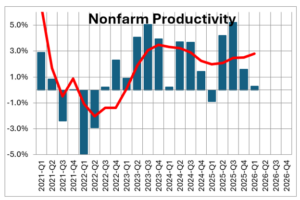

- Second-quarter GDP growth is projected to exceed 3%, supported by stronger manufacturing activity and AI-driven productivity gains.

- Core CPI inflation remains at 2.7%, above the Federal Reserve‘s 2% target.

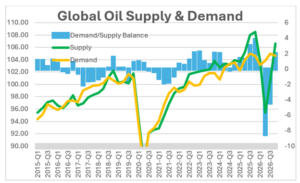

- Oil prices and inflation risks hinge on whether commercial traffic resumes through the Strait of Hormuz.

If there was any doubt, the employment report for May confirmed that the economy is gathering momentum.

If there was any doubt, the employment report for May confirmed that the economy is gathering momentum.

Following a year when employment was barely climbing, jobs growth in recent months has quickened to about 180,000. The long dormant manufacturing sector has turned upwards. Second quarter GDP growth is likely to exceed 3.0%. Meanwhile the core CPI inflation rate continues to climb at a 2.7% pace which is still well in excess of the Fed’s 2.0% inflation target.

That GDP growth/inflation combo has made market participants nervous and they currently expect the Fed to tighten 0.25% by yearend. Whether that happens or not will depend to a large extent on re-opening of the Strait of Hormuz.

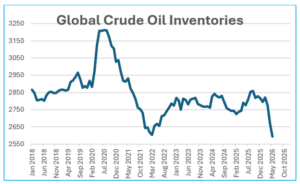

If the Strait re-opens to commercial traffic oil prices will fall and the inflation problem will largely go away. But if it doesn’t re-open soon oil prices and inflation will worsen and force the Fed into tightening mode. That is because right now oil demand far outpaces supply and global oil inventories have shrunk to a record low level and are declining every month.

If the Strait remains effectively closed oil prices will steadily climb and boost the inflation rate further. The key to avoiding this situation is a resumption of the flow of oil through the Strait of Hormuz.

Payroll employment for May rose 172,000. In the past three months employment gains have averaged 188,000 per month. That is in sharp contrast to the average monthly gain of just 10,000 in 2025. Business leaders and consumers have largely shrugged off higher tariffs, deportation of illegal immigrants, federal government layoffs, the prolonged end-of-year government shutdown, and the war with Iran that began in late February.

The fear late last year was that the economy was on the cusp of recession. That has yielded to a concern that the economy is gathering momentum and higher rates will be needed in the months ahead to cool things down.

The problem is not with the acceleration in GDP growth. That is being driven by spending on technology in general, AI in particular. As a result productivity growth has surged in the past year to 2.8% after having risen a meager 1.2% in the previous 10 years.

The gain in productivity has boosted the economy’s speed limit from 2.0% to about 3.0%. That means that the economy can safely grow at a sustained 3.0% pace without putting upward pressure on the inflation rate. With GDP growth in the past year of 2.5% the economy is not yet exceeding the speed limit. No problem on the growth front.

Inflation is a different story.

The war with Iran has caused gasoline prices to jump 50% from about $3 per gallon prior to the war to $4.50.

The rise in gasoline prices has caused the overall CPI inflation rate to climb from 2.5% to 3.8%. The core rate (excluding the volatile food and energy components) thus far has not been significantly affected. It was running at about 2.5% prior to the war versus 2.7% currently. The inflation problem is all oil-related which takes us to the Strait of Hormuz.

From 1980 until his retirement in 2003, Stephen Slifer served as chief U.S. economist for Lehman Brothers in New York City, directing the firm’s U.S. economics group along with being responsible for forecasts and analysis of the U.S. economy. He has written two books on using economic indicators to forecast financial moves and previously served as a senior economist at the Board of Governors of the Federal Reserve in Washington, D.C. Slifer can be reached at www.numbernomics.com.

e