Upcoming Event

Free Newsletter

Free Newsletter

Dollar and Euro banknotes overlaid with barcode abstract

Dollar and Euro banknotes overlaid with barcode abstract

Something is still not right

Stephen Slifer // April 29, 2026//

- Consumer confidence at record lows despite steady GDP growth

- Inflation has raised prices 13% above Fed target trajectory

- Income gap drives divide between high and low earners

- Rising costs for necessities hit lower-income families hardest

The economy is chugging along with GDP growth of about 2.0% despite a number of headwinds. The unemployment rate is 4.3%, so everybody who wants a job has one. On the surface, the economy is doing relatively well. But consumer confidence is at a record low level. How can that be? What can be done to boost consumer spirits?

The economy is chugging along with GDP growth of about 2.0% despite a number of headwinds. The unemployment rate is 4.3%, so everybody who wants a job has one. On the surface, the economy is doing relatively well. But consumer confidence is at a record low level. How can that be? What can be done to boost consumer spirits?

Consumer confidence by any measure is at a record low level.

But at the same time, consumers continue to spend quite freely. Historically, that should not happen. When consumers get nervous, they typically cut back on spending. They make that old clunker last another year or two. No fancy overseas vacation. Eat out at a restaurant less often. Why isn’t that happening this time?

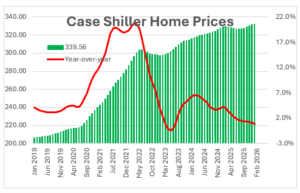

The answer is that we are creating an increasingly bifurcated economy as the income gap between upper and lower income families has widened dramatically. Those at the top have benefitted from the dramatic rise in both stock prices and the value of their home. The S&P 500 index has risen 25% in the past year to a record high level.

Home prices have risen 50% in the past five years.

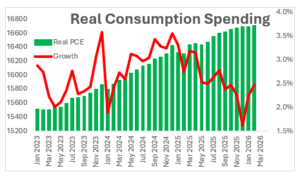

If you happen to own your own home and have a stock portfolio, you are quite content. The 43% of American families making more than $100,000 annually appear to be using stock market gains to support their lifestyle and keep consumer spending climbing at a moderate pace.

But the other 57% of American families making less than $100,000 are concerned. They do not earn enough to purchase a median-priced house. They may have student loan and car payments to make. They have no money left over at the end of the month to buy stocks. They are struggling. The primary reason for their worry is that inflation has eroded their purchasing power, and that is unlikely to change. Tariffs will continue to be passed through to consumers. The war has boosted gas prices. And now AI may soon replace their job.

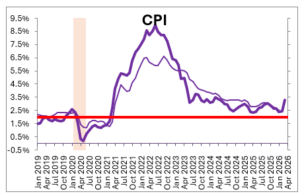

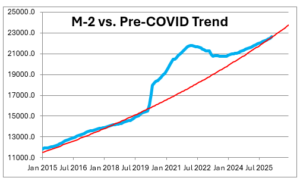

Consumer problems began when inflation accelerated in 2021 and 2022. It had been chugging along at about a 2.0% pace but suddenly surged to 9.0%. The Fed insisted that the increase was “temporary.” To an economist, a temporary increase is what happens to food prices if there is a drought, or to gasoline prices if a hurricane shutters refineries and curtails production in the Gulf of Mexico. Prices go up initially, but eventually fall to roughly where they started. That did not happen. Prices rose but never declined. They continued to climb, but at a slower pace.

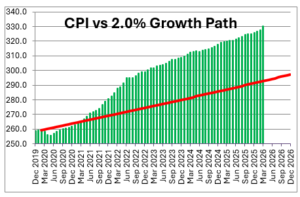

The Fed wanted prices to rise 2.0% in each of the past seven years. Instead, the average increase in the CPI during that period was 3.9%, almost twice as fast as the Fed intended. And the impact is cumulative. Each year that inflation exceeds the 2.0% target, the actual price gets farther and farther above where it should be. Currently, prices for the items in the CPI basket of goods and services are 13% higher than they would have been if inflation had risen at a 2.0% pace. No wonder consumers are complaining.

For lower-income American families, the “excessive” price gains have been concentrated on necessities — rent, food, gas prices, automobile insurance and repairs. The “excessive” price gain for all items in the CPI is 13%. But prices for necessities have risen far more rapidly. The charts for specific items all look similar, but a couple of examples will suffice. One pound of ground beef seven years ago was $3.86. Today it is $6.70. Working through the math, today’s price is 54% higher than it would have been if prices had risen 2.0% annually. Coffee was $4.05. Today it is $9.60. Today’s price is 112% higher than it would have been with a 2.0% price gain annually. Other “excessive” price increases include gasoline +31%, car insurance +38%, car repairs +47%, rent +17%. Prices of necessities have risen far more rapidly than the prices of other items in the CPI index.

Unfortunately, lower-income families cannot avoid the pain. They need to pay the rent. They need to eat. They need to fill the car with gas, pay automobile insurance and do necessary repairs to get to work every day. Their lives are often filled with hard choices. Skip the rent payment in order to buy food so the kids can eat? Fill the car with gas or take the bus to work? No wonder consumer confidence is so low. Those who can least afford it are getting hit the hardest.

This does not mean the economy is in danger of falling into recession. The 43% of middle- and upper-income American families who are benefitting from the run-up in stock prices and the value of their home should continue to spend at a fast enough pace to keep overall consumer spending climbing at a moderate pace of about 1.2% this year. And the continuing adoption of AI should keep investment spending humming at a rapid 6.0% rate.

Having said that, it is not a good situation when 57% of American families are stretching their paycheck to cover monthly expenses, are unable to purchase a house and fear what the economy might look like a few years down the road.

Confidence, once lost, is hard to restore. In a recession, confidence slides, but when the recession ends, it will rebound. This is different.

The inflation surge that pushed prices sharply higher was the catalyst for the problems faced by so many American families today. It was caused when the Fed misread the economy. It strongly believed the run-up in inflation would be temporary and, as a result, it began to raise rates 18 months later than it should have, which allowed higher prices to become embedded in the economy. The Fed has since eliminated all of the surplus liquidity it created earlier. If it maintains its current 5% growth rate in the money supply, the inflation rate should slowly shrink toward the Fed’s desired 2.0% pace, but it may not get there until 2027. Meanwhile, the Fed will get a new chair, Kevin Marsh, next month, and he plans to substantially alter the way the Fed operates. Who knows what might happen to money growth then.

Another complicating factor is the surge in oil prices caused by the war. If oil prices remain around $100 per barrel for some time, those higher prices will eventually seep into a wide variety of goods that use oil as an input in the production process, such as plastics, synthetic fibers for clothing, asphalt for roads, roofing shingles and personal care and beauty products. In that case, the inflation rate will not shrink from its current 3.0% pace anytime soon.

The other source of angst for consumers is the scattershot way that fiscal policy has been carried out. Tariffs were imposed shortly after the administration took office last year. But the rates, the countries impacted and the goods to which they applied all changed with considerable frequency. Efforts to deport undocumented immigrants, reductions in the federal workforce and government shutdown disruptions have added to uncertainty. And now there is the war with Iran.

Nobody can predict with any degree of confidence what might happen next. All Americans are nervous, but especially those at the lower end of the income scale who are living paycheck to paycheck.

It is hard to see an end to the chaotic implementation of fiscal policy anytime soon. The current administration still has time remaining in office, and its approach to policymaking is unlikely to change significantly. Even if Congress shifts control, executive actions will likely continue to drive policy direction.

We would like to see Americans feel more confident about their future. But inflation will remain above target for some time, and uneven fiscal policy is likely to continue. Confidence should eventually rebound, but not anytime soon.

From 1980 until his retirement in 2003, Stephen Slifer served as chief U.S. economist for Lehman Brothers in New York City, directing the firm’s U.S. economics group along with being responsible for forecasts and analysis of the U.S. economy. He has written two books on using economic indicators to forecast financial moves and previously served as a senior economist at the Board of Governors of the Federal Reserve in Washington, D.C. Slifer can be reached at www.numbernomics.com.

i