Upcoming Event

Free Newsletter

Free Newsletter

(Photo/DepositPhotos)

(Photo/DepositPhotos)

Inflation — not as bad as you think

Guest Columnist // June 18, 2026//

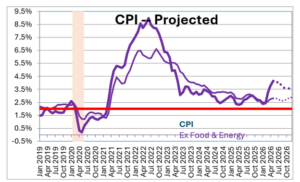

- The Consumer Price Index rose 4.2% year over year in May, the fastest pace since 2023.

- Economist Stephen Slifer says the current inflation increase is largely driven by higher energy and gasoline prices.

- Money supply growth remains subdued, unlike the rapid expansion that fueled inflation during 2020-2022.

- Slifer expects inflation to moderate once energy prices decline and geopolitical tensions ease.

The CPI continued to climb in May with the year-over-year increase now at 4.2% — the fastest pace since 2023. That sounds ominous. But the current inflation jump is totally unlike what happened to inflation in the wake of the 2020 recession — and not as threatening.

The CPI continued to climb in May with the year-over-year increase now at 4.2% — the fastest pace since 2023. That sounds ominous. But the current inflation jump is totally unlike what happened to inflation in the wake of the 2020 recession — and not as threatening.

Six years ago measures designed to combat COVID pushed the economy into a short but very steep recession. The Fed responded by purchasing Treasury securities in an effort to revive the economy. Money supply growth surged. The economy was flooded with surplus liquidity and the inflation rate soared. Worse yet, the Fed was 1-1/2 years late in beginning to eliminate the surplus liquidity which allowed the initial runup in inflation to become entrenched.

That is not happening today for two reasons. First, the current increase in prices is almost all oil related. Second, growth in the money supply is subdued which means that the run-up in inflation this time will be narrowly based and muted. Once the war ends — whenever that may be — oil prices will fall, the inflation rate will slow markedly and eventually return to the desired 2.0% pace.

The increase in inflation this time is much more likely to be “temporary” than it was previously. There is no need for the Fed to raise rates to slow the economy and force the inflation rate lower. That will happen on its own accord once the war ends. Having said that, we expect the Fed to adopt a tightening bias at its meeting this week to show that it is prepared to respond if oil prices rise further and/or prices of other goods begin to climb. Given its policy mistake in 2021-2022, the Fed needs desperately to maintain its credibility.

The CPI inflation rate has risen sharply in each of the three months since the war began at the end of February. The year-over-year increase stands at 4.2%, but it has risen at a breathtaking 8.0% pace in the past three months. It is beginning to look similar to what happened between 2020-2022. But what is happening today is totally different from what happened then.

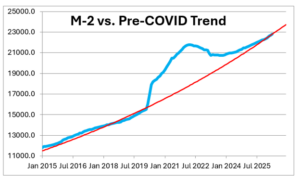

In early 2020 COVID was spreading rapidly. To prevent its spread, lockdown orders were issued in many parts of the country and travel restrictions were put in place. As a result, the economy slipped into the deepest economic downturn since the Great Depression. In an effort to re-invigorate the economy, the Fed quickly began buying U.S. Treasury and mortgage-backed securities. That caused money supply growth to soar. It continued to purchase securities until March 2022, at which point the money supply was $4.0 trillion above its usual 6.0% growth path. That means that there was $4.0 trillion of surplus liquidity circulating in the economy. No wonder the inflation rate soared!

The Fed insisted that the acceleration in inflation was temporary. It was wrong. The inflation rate did not subside because the Fed had provided far too much liquidity. The Fed did not recognize its problem until March 2022 when it began to shrink its balance sheet. The CPI inflation rate peaked at 9.0% three months later.

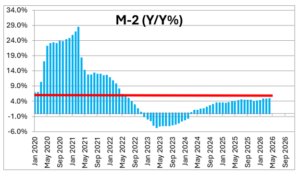

The inflation boost today is completely different from what was described above and its impact on the economy will be unlike that earlier experience. In the past year money supply growth has been 4.7%, which is slower than its historical 6.0% pace and not even in the ballpark with the 20-25% growth rates registered in 2020 and 2021.

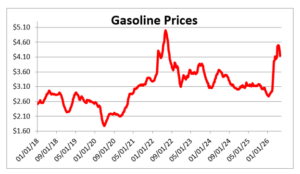

In contrast to the 2020-2022 period, there is no surplus liquidity in the economy today and, hence, no reason to expect a sustained increase in the inflation rate. Rather, the current increase in prices has been almost exclusively related to energy. The war with Iran has caused gasoline prices to jump 50% from $3.00 per gallon prior to the war to $4.50. The increase in gas prices has accounted for about 80% of the increase in the CPI in the past three months. The core inflation rate (excluding food and energy prices) has accelerated only slightly from 2.6% at the end of last year to 2.8% currently.

We are dealing almost exclusively with a rapid acceleration in the price of energy, gasoline in particular. It is not the broad-based increase in the inflation rate of five years ago, the seeds for which were planted by the Fed. If money growth continues at a subdued pace in the months ahead, we will not be dealing with a sustained increase in inflation.

From 1980 until his retirement in 2003, Stephen Slifer served as chief U.S. economist for Lehman Brothers in New York City, directing the firm’s U.S. economics group along with being responsible for forecasts and analysis of the U.S. economy. He has written two books on using economic indicators to forecast financial moves and previously served as a senior economist at the Board of Governors of the Federal Reserve in Washington, D.C. Slifer can be reached at www.numbernomics.com.

n