Upcoming Event

Free Newsletter

Free Newsletter

(Photo/DepositPhotos)

(Photo/DepositPhotos)

Inflation is slowing – what should the Fed do?

Stephen Slifer // June 30, 2026//

- Crude oil prices have fallen sharply, pushing gasoline prices lower and easing inflation pressures.

- The decline in fuel costs could contribute to lower CPI readings in June and July.

- Economist Stephen Slifer still expects the Federal Reserve to raise interest rates by 0.25% to reinforce its inflation-fighting credibility.

- Slifer forecasts inflation could fall to about 2.5% by year-end while economic growth remains resilient.

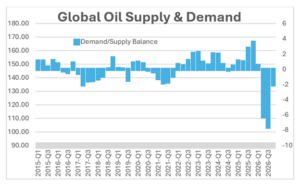

Oil prices have plunged in the past month. That was not supposed to happen. Energy experts expected the demand/supply oil imbalance to continue through the end of the year, which suggested higher prices ahead and the global inventory shortage to become more acute.

Oil prices have plunged in the past month. That was not supposed to happen. Energy experts expected the demand/supply oil imbalance to continue through the end of the year, which suggested higher prices ahead and the global inventory shortage to become more acute.

But crude prices have plunged to within shouting distance of their pre-war level. Pump prices have reversed about one-third of their war-related runup, with further declines in store. The drop in gas prices will filter into the overall CPI reading for June and July, with no change or even declines in the readings for each of those two months.

At its meeting last week, the Fed stated that it was committed to returning inflation to its 2.0% target pace, and 17 of 18 FOMC participants expected the funds rate to climb 0.25% prior to the end of the year. But now, in the face of a significant change in the inflation calculus, will the Fed actually raise rates? Ordinarily we would say no.

Growth is relatively robust, the unemployment rate is essentially at its full-employment threshold, and inflation is headed lower. In our opinion, there is no compelling economic reason to do so.

Nevertheless, we expect the Fed to raise the funds rate 0.25%. Why? Because the Fed needs to bolster its credibility. Inflation has been higher than the Fed’s 2.0% target for the past five years, and its unwillingness to tighten in 2021-2022 until about 1-1/2 years too late severely damaged its credibility. A 0.25% increase in the funds rate will do little damage to the economy, but it will demonstrate that the Fed is finally serious about achieving its 2.0% inflation goal.

Once the war broke out at the end of February, OPEC oil production plummeted. Demand far exceeded supply. The global shortage is currently about 6.0 million barrels per day. Production through the Strait of Hormuz has recently picked up to 60-65 ships per day, which is significantly higher than the near-zero transits when the Strait was completely blocked. But it is still far below the 135-140 passages daily prior to the war. It will take time for those ships that are able to transit the Strait to reach their destination, unload and get that oil to its final destination.

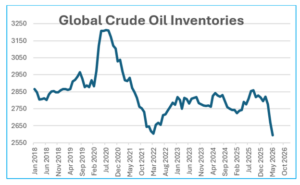

As a result of the supply shortfall, every country has dipped into its crude oil stockpile. Global inventories have fallen to a critical level, and if the demand/supply imbalance continues, oil experts suggest that prices will climb sharply. That is the theory.

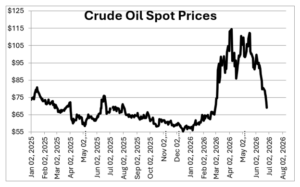

But the reality is that oil prices have plunged since the first ceasefire was announced in early April. After reaching a peak of $115 per barrel, crude has declined to $70. Prior to the war, it was $65 per barrel.

Pump gasoline prices have fallen 15% from a peak of $4.45 per gallon to $3.90, and spot prices have fallen even more sharply, which suggests that pump prices should continue to decline. Prior to the war, they started at $3.00.

Traders apparently expect the ceasefire to hold despite periodic clashes along the way and production to climb gradually in the months ahead. They may have gotten somewhat ahead of reality, but the trend seems clear. Oil production is poised to climb, oil inventories will rebound and prices will decline further.

Given what has already happened to gasoline prices, the CPI is likely to decline somewhat in June, with a further small drop in July. For what it is worth, we expect the overall CPI to decline 0.5% in June and the core CPI to increase by 0.2%.

If we see an additional small drop in July, the overall CPI should slow from 4.2% currently to 2.5% or so by the end of the year. The core CPI should not be significantly affected by oil prices, but many products like plastics, synthetic fibers and tires use oil in the production process, so there could be a slight downward bias to the core CPI reading as well. We expect the core CPI to edge down from 2.8% today to 2.7% by year-end.

So what should the Fed do?

GDP growth seems solid. We saw 2.1% growth in the first quarter. We expect 2.6% in the second quarter. And with jobs climbing by about 100,000 per month and wages rising, nominal income growth should begin to climb more quickly.

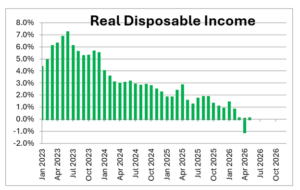

If the CPI declines for a month or two, real disposable income should rise fairly sharply from no growth in the past year to about 2.0% by year-end. If that happens, GDP growth should remain robust at about a 2.5% pace in the second half of the year.

With jobs growth of 100,000 per month, the unemployment rate should hold at 4.3%, which is virtually identical to its full-employment threshold of 4.2%.

The inflation rate seems likely to slow from 4.2% currently to 2.5% by year-end, and the core rate could edge lower from 2.8% to 2.7% by the end of the year. Inflation remains above target, but much closer to where it should be going forward than it does now. We do not think there is a compelling economic reason to tighten any time soon.

However, Fed credibility was shattered by its major policy error in 2021 and 2022. Inflation soared when the brief two-month recession ended in April 2020 as the economy roared back to life and manufacturers were unable to boost production quickly enough to keep pace. Supply shortages emerged. Inflation soared.

The Fed insisted that the runup in inflation was temporary. It was not. Because the Fed did not tighten quickly, the dramatic rise in prices became embedded in the economy. Inflation continued to rise, but at a slower rate. It never declined. Given its dramatic policy faux pas, the Fed lost considerable credibility. For that reason, we believe the Fed will raise rates 0.25% between now and year-end. This new Fed needs to demonstrate that it is serious about reducing inflation to the targeted 2.0% pace. A rate hike could do the trick.

From 1980 until his retirement in 2003, Stephen Slifer served as chief U.S. economist for Lehman Brothers in New York City, directing the firm’s U.S. economics group along with being responsible for forecasts and analysis of the U.S. economy. He has written two books on using economic indicators to forecast financial moves and previously served as a senior economist at the Board of Governors of the Federal Reserve in Washington, D.C. Slifer can be reached at www.numbernomics.com.

i