Upcoming Event

Free Newsletter

Free Newsletter

Economist Stephen Slifer warns that rising federal deficits, growing debt and looming Social Security funding challenges require action before the nation's fiscal outlook worsens. (Photo/DepositPhotos)

Economist Stephen Slifer warns that rising federal deficits, growing debt and looming Social Security funding challenges require action before the nation's fiscal outlook worsens. (Photo/DepositPhotos)

US budget deficit, debt threaten economic future

Stephen Slifer // July 13, 2026//

- The federal budget deficit is projected to reach $1.8 trillion in fiscal 2026 and exceed $3 trillion within a decade.

- The Social Security Trust Fund is projected to be depleted by the fourth quarter of 2032, triggering a 22% reduction in benefits under current law.

- Federal spending, particularly entitlement programs and interest on the national debt, is identified as the primary driver of rising deficits.

- Interest payments on the national debt have grown to $970 billion annually, surpassing defense spending.

We have written about the war and oil prices, inflation and the Fed for weeks. Time to switch gears and take a look at the budget deficit for the next decade.

We have written about the war and oil prices, inflation and the Fed for weeks. Time to switch gears and take a look at the budget deficit for the next decade.

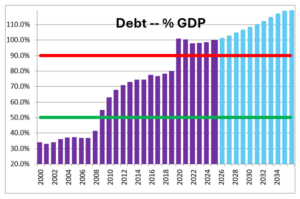

Both the budget deficit and Treasury debt outstanding as a percent of GDP are already at record high levels and will continue to climb for the next decade. Interest on the public debt as a percent of GDP will surge.

This is not a sustainable solution. But Congress continues to ignore the issue. It will not go away. At the same time the Social Security Trust Fund will have evaporated by the fourth quarter of 2032. Six years from now. Once that happens the monthly benefits checks to all 62 million Social Security recipients will be cut by 22%. This issue will also not go away and, once again, no one in Congress seems concerned. The clock is ticking. Every year of inaction means that the ultimate adjustment required to solve the problems will be increasingly onerous. Nobody cares.

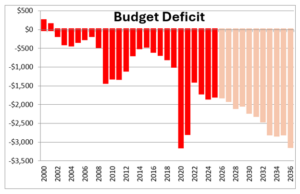

The budget deficit for fiscal 2026 should be $1.8 trillion. The last budget surplus was in 2001. That was 25 years ago. The budget exploded during the 2008-09 recession and surged again in the COVID-related recession in 2020.

Within a decade it is projected to exceed $3.0 trillion and that will occur only if there is no recession between now and then. That seems unlikely. During a recession tax revenues shrink and government spending explodes. We saw what happened in 2008-09 and 2020. We should assume that the $3.0 trillion deficit projected for 2036 will be a best-case scenario — unless Congress does something.

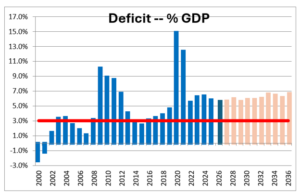

Perhaps the best way to evaluate any budget deficit is as a percent of GDP. If the economy can grow quickly enough perhaps these seemingly outsized deficits are affordable. Unfortunately, viewed in that way the deficits are still a problem. Over the 60 years between 1960 and 2020 the budget deficit as a percent of GDP averaged about 3.0%. Economists view a deficit of that magnitude as “sustainable.” But for the current fiscal year the deficit is likely to be 5.6% of GDP. By 2036 it is expected to climb to 6.7% of GDP. That is not even close to what economists view as sustainable.

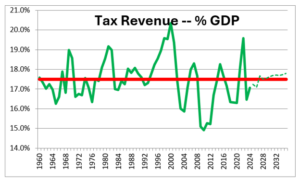

A budget deficit by definition is the shortfall between tax revenues and government spending. Which of the two is more responsible for the deficit explosion? Answer: government spending.

Historically, tax revenues average about 17.5% of GDP. This year tax receipts should be about 17.2% and they are projected to climb to 17.8% by 2026. The budget deficits are not being caused by a shortage of tax revenue. Higher taxes are not the solution.

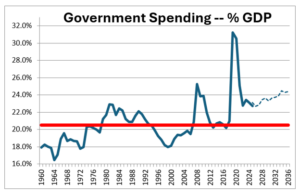

The problem is on the government spending side. Historically, spending has averaged 20.5% of GDP. This year it will be 22.7% of GDP and likely to climb to 24.4% by 2026.

The biggest problem on the spending side is that two-thirds of every dollar spent is an “entitlement,” which is a monthly income support payment. There are a wide variety of such expenditures but the largest and most widely recognized are Social Security, Medicare and Medicaid, followed by welfare spending, child support payments and veterans’ benefits.

Politicians love entitlements, which increase income for some voters in their district. For that reason entitlements almost never go down. As a result, they have climbed from 25% of the government spending pie in the mid-1950s to about 60% today and are unlikely to decline much any time soon. For a politician a vote to cut Social Security payments will almost certainly be the train wreck that ends their career.

An additional problem on the spending side is interest on the public deficit. At $970 billion it is now the third-largest expenditure category after Social Security, which costs $1.6 trillion, and Medicare at $1.2 trillion. Interest on the debt exceeds defense spending, which is $898 billion. As a percent of GDP it is the highest since the government began keeping records in 1940, and it is going to keep climbing in the years ahead as the debt level grows and interest rates remain steady.

From 1980 until his retirement in 2003, Stephen Slifer served as chief U.S. economist for Lehman Brothers in New York City, directing the firm’s U.S. economics group while also being responsible for forecasts and analysis of the U.S. economy. He has written two books on using economic indicators to forecast financial markets and previously served as a senior economist at the Board of Governors of the Federal Reserve in Washington, D.C. Slifer can be reached at www.numbernomics.com.