Upcoming Event

Free Newsletter

Free Newsletter

New Federal Reserve Chair Kevin Warsh faces his first major policy decision as inflation pressures and economic growth shape expectations for interest rates. (Photo/DepositPhotos)

New Federal Reserve Chair Kevin Warsh faces his first major policy decision as inflation pressures and economic growth shape expectations for interest rates. (Photo/DepositPhotos)

Fed expected to hold rates as inflation concerns persist

Stephen Slifer // June 2, 2026//

- Kevin Warsh has begun his term as Federal Reserve chair amid debate over interest rates.

- Analysts expect the Fed to drop its easing bias at the June meeting and signal a tougher stance on inflation.

- GDP growth, consumer spending and AI-driven productivity gains continue to support the economy.

- Rising energy prices linked to the Iran conflict have pushed headline inflation higher.

Kevin Warsh has begun his term as Fed chair. His predecessor, Jay Powell, frequently clashed with Trump regarding the appropriate level of interest rates. Trump argued that a “neutral” level for the funds rate was about 1.0%. The FOMC believed that the “neutral” rate was about 3.0%. Trump made it clear that his nominee for Fed chair would be expected to lower interest rates.

Kevin Warsh has begun his term as Fed chair. His predecessor, Jay Powell, frequently clashed with Trump regarding the appropriate level of interest rates. Trump argued that a “neutral” level for the funds rate was about 1.0%. The FOMC believed that the “neutral” rate was about 3.0%. Trump made it clear that his nominee for Fed chair would be expected to lower interest rates.

Will Warsh cave to pressure from Trump to lower rates even if they are unnecessary? We do not think so. The economy today is stronger and the inflation rate much higher than it was in the spring when Warsh testified. We believe that on June 17 the Fed will lose its current easing bias and replace it with a bias toward tightening. Such action would reassure bond market participants that the Fed will not repeat its 2021-2022 mistake of waiting too long to raise interest rates.

The stock market continues to climb. Investors initially got nervous about the war with Iran which triggered a long-awaited correction, but the market rebounded quickly and has set a series of record high levels in recent months.

The stock market continues to climb. Investors initially got nervous about the war with Iran which triggered a long-awaited correction, but the market rebounded quickly and has set a series of record high levels in recent months.

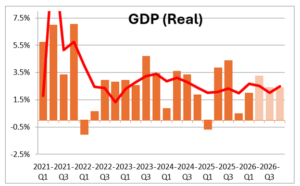

GDP growth in the first quarter came in slightly higher than expected at 2.0%. Second quarter growth seems likely to exceed 3.0%.

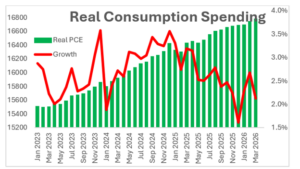

Growth is being supported by consumer spending which continues to climb at a 2.1% pace even though consumer confidence is at a record low level. Middle and upper income consumers are dipping into stock market gains to maintain their lifestyle.

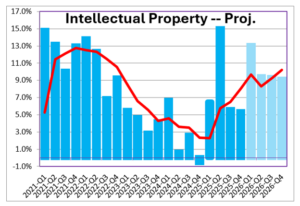

At the same time the AI boom has caused the intellectual property component of investment spending to climb at a robust 10% pace.

At the same time the AI boom has caused the intellectual property component of investment spending to climb at a robust 10% pace.

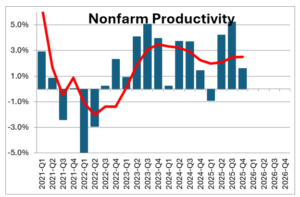

AI is also boosting productivity growth which further bolsters GDP growth. Between 2000 and the beginning of the 2020 recession productivity growth averaged 2.0%. In the past three years productivity has climbed at a 2.8% rate. As a result, our economic speed limit has climbed from 2.0% to about 3.0%.

Meanwhile, jobs are once again being created. Payroll employment was essentially unchanged each month in 2025, but is now rising by about 75,000 per month. At the same time the unemployment rate is 4.3% which is its “full employment” level. Everybody who wants a job has one.

Meanwhile, jobs are once again being created. Payroll employment was essentially unchanged each month in 2025, but is now rising by about 75,000 per month. At the same time the unemployment rate is 4.3% which is its “full employment” level. Everybody who wants a job has one.

On the inflation front the war has boosted gasoline prices from $3.10 per gallon prior to its start to $4.50 per gallon.

The overall CPI index has surged as higher gas prices have boosted it to 3.8%. The core rate is a different story. Prior to the war the core CPI was stuck at about 2.5%. It has since climbed to 2.7%. The recent runup in inflation has almost all been energy related.

With the stock market at a record high level, GDP growth at its potential pace, the labor market at full employment, and the core inflation rate slightly above target, what should the Fed do?

With the stock market at a record high level, GDP growth at its potential pace, the labor market at full employment, and the core inflation rate slightly above target, what should the Fed do?

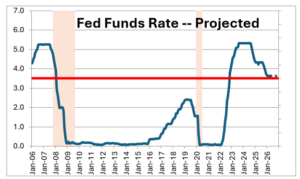

The Fed believes the funds rate is neutral when it is at 3.0% although many FOMC members think it could be higher. We agree and believe the funds rate is neutral when it is about 3.5%. The funds rate currently is 3.6%. Short rates are about where they should be. Nobody other than Trump believes the neutral rate is 1.0%.

The Fed only has control over short-term interest rates. It cannot determine long-term rates which are driven primarily by inflation. The yield on the Treasury’s 10-year note has risen from 4.1% at the end of last year to 4.5% which reflects the near-term impact on inflation caused by the war and higher oil prices. Longer-term inflation expectations have been quite stable.

The Fed only has control over short-term interest rates. It cannot determine long-term rates which are driven primarily by inflation. The yield on the Treasury’s 10-year note has risen from 4.1% at the end of last year to 4.5% which reflects the near-term impact on inflation caused by the war and higher oil prices. Longer-term inflation expectations have been quite stable.

Ten-year inflation expectations, as measured by the difference between the nominal and inflation-adjusted rates on 10-year notes, is currently 2.4%. It has been at roughly that same rate for the past four years.

So what should the Fed do? At the next FOMC meeting on June 16-17 it is inconceivable that Kevin Warsh will push for a rate cut given the economic backdrop described above. Whatever his view might be about the level of a “neutral” rate longer term, this is not the time for a rate cut.

But what about the bias? The Fed continues to have an easing bias even though at the last meeting three Fed officials objected. Since that time the inflation rate has continued to accelerate and the easing bias is sure to disappear.

But what about the bias? The Fed continues to have an easing bias even though at the last meeting three Fed officials objected. Since that time the inflation rate has continued to accelerate and the easing bias is sure to disappear.

The Fed could opt for an unbiased directive and cite uncertainty caused by the war on both the economy and inflation. But the Fed has a credibility problem. Inflation has been faster than the Fed’s 2.0% target for the past five years.

Furthermore, it made a huge policy error in 2020 by not tightening sooner than it did when the economy rebounded vigorously from the recession. To adopt a tightening bias would send a message that the Fed is serious about returning inflation to the 2.0% mark. With the market expecting a 0.25% rate hike by year-end, anything short of a tightening bias might send a message that the Fed is still not serious about fighting inflation which would likely push the yield on the 10-year note to or above the 5.0% mark.

Furthermore, it made a huge policy error in 2020 by not tightening sooner than it did when the economy rebounded vigorously from the recession. To adopt a tightening bias would send a message that the Fed is serious about returning inflation to the 2.0% mark. With the market expecting a 0.25% rate hike by year-end, anything short of a tightening bias might send a message that the Fed is still not serious about fighting inflation which would likely push the yield on the 10-year note to or above the 5.0% mark.

From 1980 until his retirement in 2003, Stephen Slifer served as chief U.S. economist for Lehman Brothers in New York City, directing the firm’s U.S. economics group along with being responsible for forecasts and analysis of the U.S. economy. He has written two books on using economic indicators to forecast financial moves and previously served as a senior economist at the Board of Governors of the Federal Reserve in Washington, D.C. Slifer can be reached at www.numbernomics.com.

F